Researchers have made great strides in improving our understanding of the effects of unconventional monetary policy. Although further study is needed, the evidence from the past few years demonstrates that both forward guidance and large-scale asset purchases are useful policy tools when short-term interest rates are constrained by the zero bound.

The following is adapted from a presentation made by the president and CEO of the Federal Reserve Bank of San Francisco to the Swiss National Bank Research Conference on September 23, 2011. The full text is available at https://www.frbsf.org/news/speeches/2011/john-williams-0923.html

Thank you for the kind introduction and for giving me the opportunity to address this very distinguished group in the beautiful city of Zurich. The Swiss National Bank’s annual research conference has established itself as one of the world’s most substantive forums for discussion of monetary policy issues. The theme selected for this year’s conference, “Policy Challenges and Developments in Monetary Economics,” is particularly timely and relevant. In the past three years, there has certainly been no shortage of policy challenges and developments in the field of monetary economics.

Chairman Bernanke (2009) said, “Extraordinary times call for extraordinary measures.” Well, extraordinary measures have been taken. In the face of severe dislocations in financial markets and deep declines in economic activity, several central banks have lowered short-term policy rates essentially to their zero lower bound. A number of central banks—including the Federal Reserve—have also used nonstandard or “unconventional” monetary policies. By that I mean efforts to influence interest rates and economic activity using tools other than the short-term policy rate.

Before the financial crisis, most everything we knew about unconventional monetary policy came from studies of Japan’s Lost Decade and a few scattered episodes in the United States. Now, as a result of the events of the past three years, we have numerous examples of unconventional monetary policy to study. Tonight I’d like to review some of the lessons gleaned from these experiences. I also want to highlight some of the key remaining questions regarding the implementation of such policies and their effectiveness as monetary stimulus.

In my remarks, I’ll focus on two of these unconventional monetary policy tools—forward policy guidance and large-scale asset purchases, or LSAPs in Fedspeak. There are two reasons for this focus. First, these are the policies that the Federal Reserve and other central banks have relied on most heavily over the past three years. As a result, they are also the policies that we’ve learned the most about. And second, these policies are ongoing, and therefore likely to be the most relevant for thinking about future policy. I suppose this is an opportune time to add that my remarks represent my own views and not necessarily those of others in the Federal Reserve System.

Forward policy guidance

Prior to the crisis, the theoretical literature on the zero lower bound was virtually unanimous on one point: A central bank with the ability to credibly commit to a future path of short-term interest rates could, except in the most extreme cases, circumvent the effects of the zero lower bound (see, for example, Reifschneider and Williams 2000 and Eggertsson and Woodford 2003, 2006). This conclusion stemmed from two insights. First, the output gap and inflation rate in standard textbook New Keynesian models are completely determined by long-term interest rates. They do not depend on the short-term rate, except to the extent that the long-term rate is equal to the expected path of future short-term rates. Second, if a central bank can credibly commit to future policy actions, it can continue to control longer-term interest rates, even when the short-term rate is at the zero lower bound. It can do so by managing expectations about the future path of short-term rates. Thus, in theory, forward guidance about the future path of policy is a potentially powerful tool that can almost completely solve a central bank’s problems at the zero lower bound.

However, there are reasons to be skeptical that forward guidance would be such a panacea in practice. One of these caveats is implicit in the theory itself. The optimal forward guidance policy is not time-consistent. According to the theory, for this policy to have the desired effects, the central bank must commit to two things: keeping the short-term policy rate lower than it otherwise would in the future, and allowing inflation to rise higher than it otherwise would. However, when the time comes for the central bank to fulfill this commitment, it may not want to do so. It might find it hard to resist the temptation to raise rates earlier than promised to avoid the rise in inflation (see Adam and Billi 2007). Indeed, policymakers have generally shied away from policies that promise temporarily high inflation in the future, such as price level targeting, that are in theory effective at circumventing the zero bound. This reluctance arises in part out of a concern that such an approach could unmoor inflation expectations (Evans 2010 is an exception; see Walsh 2009).

A second caveat to the power of forward guidance is that the public may have different expectations of the future course of the economy and monetary policy than the central bank. The expectations channel is crucial for the effectiveness of optimal forward guidance policy. If the public has an imperfect understanding of the central bank’s intended policy path, then forward guidance may not work as well as advertised (see Reifschneider and Roberts 2006 and Williams 2006). Therefore, a key challenge for forward guidance is communicating the intended policy path to the public. Complicating this communication challenge further, optimal forward guidance is inherently state-contingent and depends on myriad factors and risk assessments. These are inherently difficult to convey to the public. Moreover, the public and the media tend to gloss over such nuances and take away simple sound bites.

There are a number of examples of central banks using forward guidance on monetary policy. A few central banks—those in New Zealand, Norway, and Sweden—provide explicit forward guidance in the form of policy rate projections. Other central banks providing guidance have limited themselves to short statements indicating the direction and time frame of future policy actions, rather than full descriptions of an intended policy path (Rudebusch and Williams 2008 provide a discussion). The Federal Reserve’s public use of phrases such as “considerable period,” “measured pace,” and “extended period” falls into this category. The Bank of Canada and the Bank of Japan have also used forward guidance regarding the timing of and conditions for rate increases.

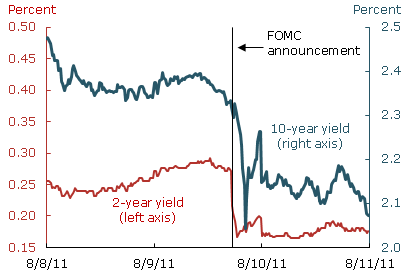

Figure 1

Intraday Treasury yields

Note: Trading data from 9:30 a.m. to 4 p.m. EDT, at five-minute intervals.

Source: Bloomberg.

Let me conclude my discussion of forward guidance by summarizing the evidence of its effectiveness. Several studies have examined the effects of central bank communication more generally (see Gurkaynak et al. 2005, Kohn and Sack 2004, and Bernanke et al. 2004). They found that the Federal Reserve’s policy statements have significant effects on financial market expectations of future policy actions and on Treasury yields. Only a few studies have looked at the effectiveness of forward guidance policies at the zero lower bound. One example was the Bank of Canada’s April 2009 statement that it expected to hold the policy rate constant until the second quarter of 2010, which had an immediate effect on financial market expectations regarding short-term interest rates. The conditionality of the guidance worked as well. When the Canadian economy appeared to be recovering from the recession more quickly than anticipated, market participants began to expect interest rates to rise ahead of the previously announced date (see Chehal and Trehan 2009).

Of course, we at the Fed have our own recent case study that speaks to the effectiveness of forward guidance. The Federal Open Market Committee’s statement issued following our August meeting said, “The Committee currently anticipates that economic conditions—including low rates of resource utilization and a subdued outlook for inflation over the medium run—are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.” As Figure 1 shows, two-year Treasury yields fell by about 0.1 percentage point and ten-year Treasury yields fell by about 0.2 percentage point following the announcement. This provides prima facie evidence of the powerful effects of forward guidance at the zero bound.

Large-scale asset purchases

Let me turn now to large-scale asset purchases, or LSAPs, the main alternative to forward guidance in the unconventional monetary policy arena today. LSAPs are central bank purchases of securities funded by an increase in reserves. Their history is older than forward guidance. It goes back at least to Operation Twist, the 1961 joint initiative of the Kennedy Administration and the Federal Reserve to purchase longer-term Treasury securities. More recently, the Bank of Japan began its so-called quantitative easing policy in 2001. It ultimately resulted in Bank purchases of almost ¥35 trillion of Japanese government bonds. In March 2009, the Bank of England announced it would purchase £75 billion of U.K. gilts, which was subsequently expanded to £200 billion. And the Federal Reserve carried out three rounds of large-scale asset purchases during the Great Recession. Two rounds of “QE1” took place in November 2008 and March 2009, during the financial crisis. The third round followed the “QE2” announcement in November 2010.

A number of theories consider the channels by which LSAPs affect Treasury yields and financial conditions more broadly (see Krishnamurthy and Vissing-Jorgensen 2011 for a thorough discussion). I will highlight two: signaling and portfolio. The signaling channel works through the effects asset purchases have on public expectations of future short-term interest rates. The portfolio channel works through the effects on factors that affect yields other than expectations of future short-term interest rates.

The basic idea of the signaling channel is that, when the central bank conducts asset purchases, it is signaling its strong intention to add monetary stimulus by other means as well. Such signaling may lower longer-term yields in two ways. First, it could lower the expected future path of short-term rates. Second, it could reduce the uncertainty around this path, which may reduce the interest rate risk associated with holding longer-term securities.

The theories underlying the portfolio channel are more diverse. In part, this is because the workhorse models of asset pricing—the representative-agent consumption CAPM model and the affine arbitrage-free model—generally do not allow the supply of a security to affect its price. In those frameworks, the supply of the asset is irrelevant for asset pricing (see Piazzesi and Schneider 2007). Instead, one has to go back to older, more eclectic theories of asset pricing, such as Tobin’s “portfolio balance” model or Modigliani and Sutch’s “preferred habitat” theory. These assume that a range of heterogeneous investors have different preferences for different asset classes and that arbitrage across these asset classes is limited. This approach has been integrated into a modern, no-arbitrage, asset-pricing framework and has been used to guide empirical analysis of LSAP effects. (See Vayanos and Vila 2009 for a recent theoretical model, and Greenwood and Vayanos 2008 and Hamilton and Wu 2011 for empirical applications.)

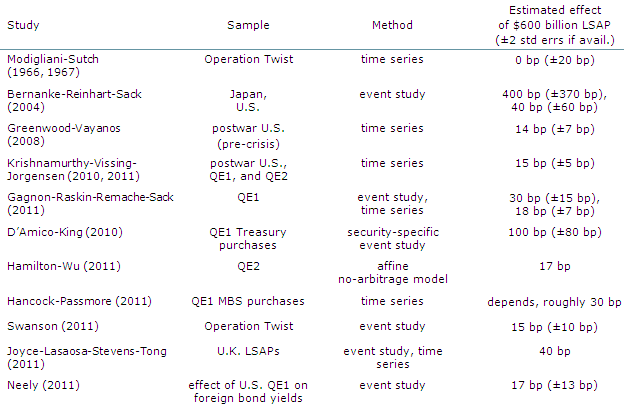

There has been a profusion of studies estimating the effects of LSAPs on asset prices. Table 1 summarizes a number of these studies. In order to facilitate comparison, the estimated effects in each analysis have been renormalized to correspond to the estimated effect on longer-term bond yields of a $600 billion LSAP operation. That, of course, was the size of the Federal Reserve’s asset purchase program completed earlier this year.

Table 1

Empirical estimates of LSAP effects

Sources: Modigliani-Sutch (1966, Sections 3-4), Bernanke-Reinhart-Sack (2004, Table 7, Figure 6, and author´s calculations), Greenwood-Vayanos (2008, Table 2), Krishnamurthy-Vissing-Jorgensen (2011, Section 4), Gagnon et al. (2011, Tables 1-2), D´Amico-King (2010, Figure 3), Hamilton-Wu (2011, Figure 11), Hancock-Passmore (2011, Table 5), Swanson (2011, Table 3), Chung et al. (Figure 10), Joyce et al. (2011, Figure 9), Neely (2011, Table 2). Almost all of these estimates involve author´s calculations to renormalize the effect to a $600 billion U.S. LSAP.

Except for a few outliers, the estimated effects on Treasury yields are remarkably close, especially when you consider the wide variety of sample periods and methods employed. Specifically, the estimated effects typically lie in the neighborhood of 0. 15 to 0.20 percentage point. Generally, the estimates are reasonably precise. Although some might argue that 0.15 to 0.20 percentage point is small, keep in mind that the typical response of the 10-year Treasury yield to a 0.75 percentage point cut in the federal funds rate is also about 0.15 to 0.20 percentage point (see Chung et al. 2011). I’ve never heard anyone argue that a 0.75 percentage point cut in the funds rate is small potatoes!

Although there is general agreement regarding the magnitude of LSAP effects on Treasury yields, there is less agreement regarding the channels LSAPs work through, as discussed in the paper by Bauer and Rudebusch (2011) presented at this conference. One way to distinguish between the signaling and portfolio channels is to examine the responses of a variety of yields and asset prices to LSAPs. If the main effect is through signaling, then we would expect a strong co-movement among all classes of longer-term yields. In contrast, a relatively muted response of assets that are not close substitutes for Treasury securities would be evidence of a portfolio effect.

The evidence is far from conclusive, but it does tentatively support some role for the portfolio channel. First, by some measures, expected short rates fell by less than government securities of equivalent maturity (see Gagnon et al. 2011 and Joyce et al. 2011). Second, there is some evidence in the literature that the pass-through from purchases of Treasury securities to private borrowing rates, such as corporate bond rates, may be relatively low (Swanson 2011, Krishnamurthy and Vissing-Jorgensen 2011, Joyce et al. 2011, Wright 2011, and Neely 2011). To the extent that this is true, it would argue against a strong signaling effect. That said, there remains a great deal of uncertainty regarding the relative importance of these channels.

Moreover, there is also uncertainty regarding how the portfolio channel actually works. In particular, to what extent is it the size or the composition of the central bank’s balance sheet that matters? This question is no mere theoretical curiosity, but has very real practical relevance. For example, it is critical for gauging the efficacy of a maturity extension program that lengthens the maturity of securities holding with no change in the quantity of holdings, such as the policy announced earlier this week by the FOMC. This program contrasts with a policy that simply increases the holdings of Treasury securities, such as the Fed’s second asset purchase program initiated late last year. The size-versus-composition question bears directly on the relative effectiveness of the two policy variants. In addition, the question is relevant for comparing the effects of a policy of purchasing Treasury securities with one of buying mortgage-backed securities.

As I have discussed, researchers have made great strides in improving our understanding of the effects of unconventional policies. The evidence from the experiences of the past few years convincingly demonstrates that both forward guidance and large-scale asset purchases are useful policy tools when short-term interest rates are constrained by the zero bound. Despite this progress, I see at least four important issues that are in need of further study. First, what are the effects of LSAPs on the overall economy? Specifically, does lowering Treasury yields through LSAPs have the same effect on the economy as an equivalent movement in the federal funds rate? Or, are the effects of LSAPs attenuated owing to limited pass-through to other asset prices or limited duration of LSAP effects? (See Baumeister and Benati 2010, Chung et al. 2011, and Wright 2011.)

Second, what approach should central banks take in formulating and communicating unconventional policies, whether forward guidance or LSAP programs? For example, what are the advantages of targeting a specific quantity of LSAPs as opposed to targeting a level or ceiling on interest rates at a particular point on the yield curve? This question is, of course, a new take on Poole’s (1970) analysis of the choice of a monetary policy instrument. And, if a quantity approach is preferable, should LSAP programs be formulated more like a policy rule rather than discrete lump-sum announcements (FRB St. Louis 2009)?

Third, should unconventional policies be a regular part of our toolkit or should they be reserved only for extraordinary times? That is, should forward guidance and LSAPs complement standard short-rate policies at all times or only at the zero lower bound? These policies are still relatively unfamiliar to the public. Consequently, their effects on the public’s inflation expectations, appetite for risk, and so forth are difficult to predict. This adds an element of uncertainty and raises concern about unintended consequences. In addition, LSAPs may create distortions to asset prices or financial market functioning. These negative effects have received scant attention in the research literature and are not well understood. Of course, these costs must be weighed against the value of asset purchases for macroeconomic stabilization.

Finally, how do these policies change our thinking about the optimal rate of inflation? In particular, if unconventional monetary policies can effectively circumvent the zero lower bound, then there is less of a need for an inflation cushion. But, if these policies cannot in practice be used as substitutes for reducing the short-term rate, then there is greater need for an inflation cushion.

These questions offer a wealth of important topics for researchers to explore. The lessons we learn from this research will be critically important when central bankers consider unconventional policies in the future. On that note, let me end with a little forward guidance: I expect we will have an extended period of policy challenges, and that developments in monetary economics will be crucial to the future success of monetary policy.

John C. Williams is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Adam, Klaus, and Roberto M. Billi. 2007. “Discretionary Monetary Policy and the Zero Lower Bound on Nominal Interest Rates.” Journal of Monetary Economics 54(3), pp. 728–752.

Bauer, Michael, and Glenn Rudebusch. 2011. “The Signaling Channel for Federal Reserve Bond Purchases.” Federal Reserve Bank of San Francisco Working Paper 2011-21.

Baumeister, Christiane, and Luca Benati. 2010. “Unconventional Monetary Policy and the Great Recession.” European Central Bank Working Paper 1258 (October).

Bernanke, Ben. 2009. “Federal Reserve Policies to Ease Credit and Their Implications for the Fed’s Balance Sheet.” Speech at the National Press Club Luncheon, National Press Club, Washington, DC, February 18.

Bernanke, Ben, Vincent Reinhart, and Brian Sack. 2004. “Monetary Policy Alternatives at the Zero Bound: An Empirical Assessment.” Brookings Papers on Economic Activity 2004-2, pp. 1–78.

Chehal, Puneet, and Bharat Trehan. 2009. “Talking about Tomorrow’s Monetary Policy Today.” 2009-35 (November 9).

Chung, Hess, Jean-Philippe Laforte, David Reifschneider, and John Williams. 2011. “Have We Underestimated the Likelihood and Severity of Zero Lower Bound Events?” Federal Reserve Bank of San Francisco Working Paper 2011-01.

D’Amico, Stefania, and Thomas King. 2010. “Flow and Stock Effects of Large-Scale Treasury Purchases.” Federal Reserve Board Finance and Economics Discussion Series 2010-52.

Eggertsson, Gauti, and Michael Woodford. 2003. “The Zero Bound on Interest Rates and Optimal Monetary Policy.” Brookings Papers on Economic Activity 2003-1, pp. 139–211.

Eggertsson, Gauti, and Michael Woodford. 2006. “Optimal Monetary and Fiscal Policy in a Liquidity Trap.” In NBER International Seminar on Macroeconomics 2004, eds. R. Clarida, J. Frankel, F. Giavazzi, and K. West. Chicago: University of Chicago Press.

Evans, Charles. 2010. “Monetary Policy in a Low-Inflation Environment: Developing a State-Contingent Price-Level Target.” Remarks delivered before the Federal Reserve Bank of Boston’s 55th Economic Conference, October 16.

Gagnon, Joseph, Matthew Raskin, Julia Remache, and Brian Sack. 2011. “The Financial Market Effects of the Federal Reserve’s Large-Scale Asset Purchases.” International Journal of Central Banking 7 (1, March), pp. 3–43.

Greenwood, Robin, and Dimitri Vayanos. 2008. “Bond Supply and Excess Bond Returns.” NBER Working Paper 13806. http://www.nber.org/papers/w13806

Gurkaynak, Refet, Brian Sack, and Eric Swanson. 2005. “Do Actions Speak Louder Than Words? The Response of Asset Prices to Monetary Policy Actions and Statements.” International Journal of Central Banking 1(1, May), pp. 55–93.

Hamilton, James, and Jing Cynthia Wu. 2011. “The Effectiveness of Alternative Monetary Policy Tools in a Zero Lower Bound Environment.” Journal of Money, Credit, and Banking, forthcoming.

Hancock, Diana, and Wayne Passmore. 2011. “Did the Federal Reserve’s MBS Purchase Program Lower Mortgage Rates?” Federal Reserve Board Finance and Economics Discussion Series 2011-01.

Joyce, Michael, Ana Lasaosa, Ibrahim Stevens, and Matthew Tong. 2011. “The Financial Market Impact of Quantitative Easing in the United Kingdom.” International Journal of Central Banking 7(3, September), pp. 113–161.

Kohn, Donald, and Brian Sack. 2004. “Central Bank Talk: Does It Matter and Why?” In Macroeconomics, Monetary Policy, and Financial Stability, proceedings of a conference held by the Bank of Canada, June 2003. Ottawa: Bank of Canada.

Krishnamurthy, Arvind, and Annette Vissing-Jorgensen. 2010. “The Aggregate Demand for Treasury Debt.” Unpublished manuscript, Northwestern University (May).

Krishnamurthy, Arvind, and Annette Vissing-Jorgensen. 2011. “The Effects of Quantitative Easing on Interest Rates.” Brookings Papers on Economic Activity, forthcoming.

Modigliani, Franco, and Richard Sutch. 1966. “Innovations in Interest Rate Policy.” American Economic Review 56 (March), pp. 178–197.

Neely, Christopher. 2011. “The Large-Scale Asset Purchases Had Large International Effects.” Federal Reserve Bank of St. Louis Working Paper 2010-018C.

Piazzesi, Monika, and Martin Schneider. 2007. “Asset Prices and Asset Quantities.” Journal of the European Economic Association 5, pp. 380–389.

Poole, William. 1970. “Whither Money Demand?” Brookings Papers on Economic Activity 1970-3, pp. 485–501.

Reifschneider, David, and John Roberts. 2006. “Expectations Formation and the Effectiveness of Strategies for Limiting the Consequences of the Zero Bound.” Journal of the Japanese and International Economies 20(3, September), pp. 314–337.

Reifschneider, David, and John Williams. 2000. “Three Lessons for Monetary Policy in a Low-Inflation Era.” Journal of Money, Credit, and Banking 32(4, November), pp. 936–966.

Rudebusch, Glenn, and John Williams. 2008. “Revealing the Secrets of the Temple: The Value of Publishing Central Bank Interest Rate Projections.” In Asset Prices and Monetary Policy, ed. J.Y. Campbell. Chicago: University of Chicago Press, pp. 247–284.

Svensson, Lars E.O. 2001. “The Zero Bound in an Open Economy: A Foolproof Way of Escaping from a Liquidity Trap.” Monetary and Economic Studies 19(S-1, February), pp. 277–312.

Vayanos, Dimitri, and Jean-Luc Vila. 2009. “A Preferred-Habitat Model of the Term Structure of Interest Rates.” NBER Working paper 15487 (November).

Walsh, Carl. 2009. “Using Monetary Policy to Stabilize Economic Activity.” In Financial Stability and Macroeconomic Policy, proceedings from the Federal Reserve Bank of Kansas City Economic Policy Symposium, pp. 245–296.

Williams, John C. 2006. “Monetary Policy in a Low Inflation Economy with Learning.” In Monetary Policy in an Environment of Low Inflation, proceedings of the Bank of Korea International Conference. Seoul: Bank of Korea.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org